Modern day alchemy, unsurprisingly, failed. A deep dive into FTX and the events leading to the collapse of the now notorious crypto exchange.

The below is an excerpt from the Bitcoin Magazine Pro report on the rise and fall of FTX. To read and download the entire 30-page report, follow this link.

The Beginnings

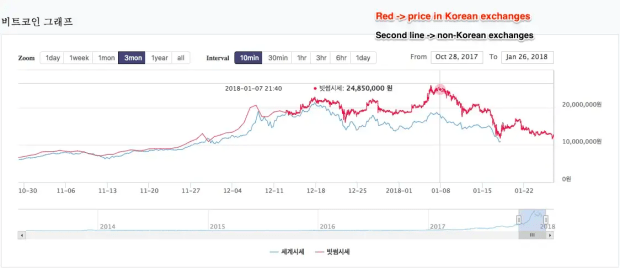

Where did it all start for Sam Bankman-Fried? As the story goes, Bankman-Fried, a former international ETF trader at Jane Street Capital, stumbled upon the nascent bitcoin/cryptocurrency markets in 2017 and was shocked at the amount of “risk-free” arbitrage opportunity that existed.

In particular, Bankman-Fried said the infamous Kimchi Premium, which is the large difference between the price of bitcoin in South Korea versus other global markets (due to capital controls), was a particular opportunity that he took advantage of to first start making his millions, and eventually billions …

At least that’s how the story goes.

The real story, while possibly similar to what SBF liked to tell to explain the meteoric rise of Alameda and subsequently FTX, looks to have been one riddled with deception and fraud, as the “smartest guy in the room” narrative, one that saw Bankman-Fried on the cover of Forbes and touted as the “modern day JP Morgan,” quickly changed to one of massive scandal in what looks to be the largest financial fraud in modern history.

The Start Of The Alameda Ponzi

As the story goes, Alameda Research was a high-flying proprietary trading fund that used quantitative strategies to achieve outsized returns in the cryptocurrency market. While the story was believable on the surface, due to the seemingly inefficient nature of the cryptocurrency market/industry, the red flags for Alameda were glaring from the start.

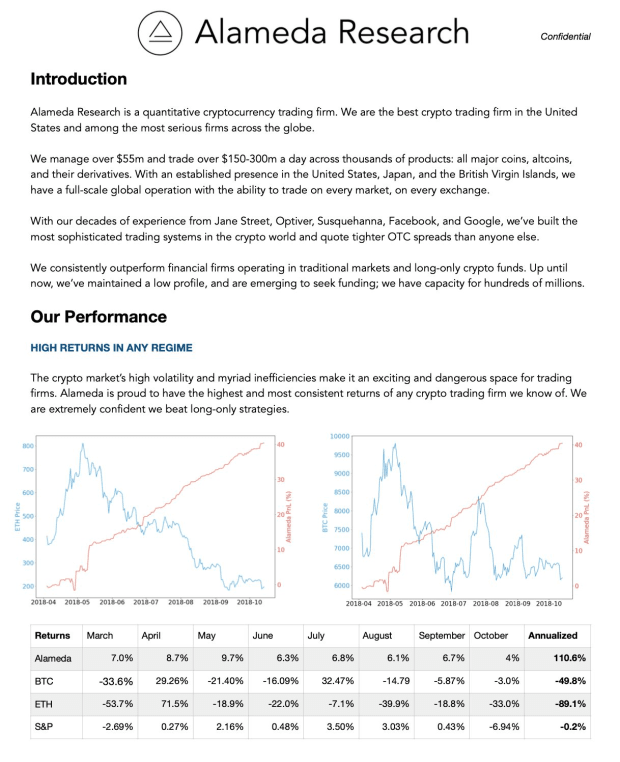

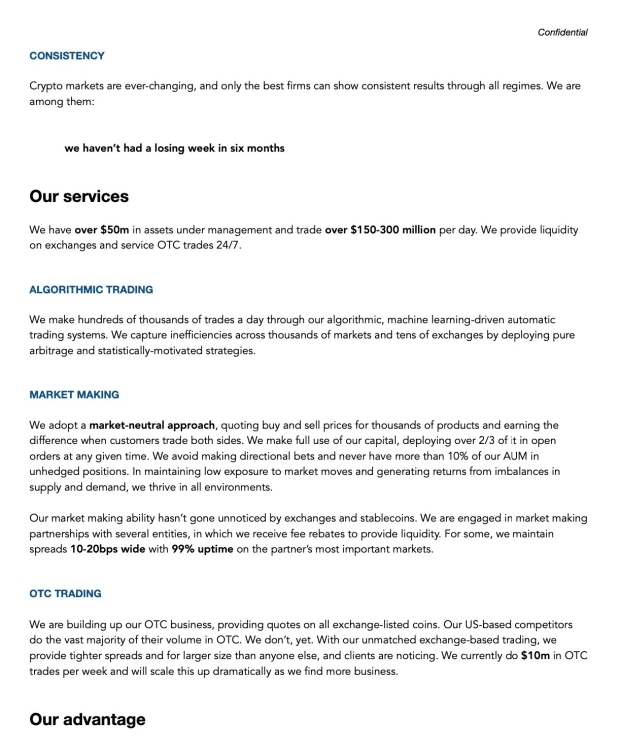

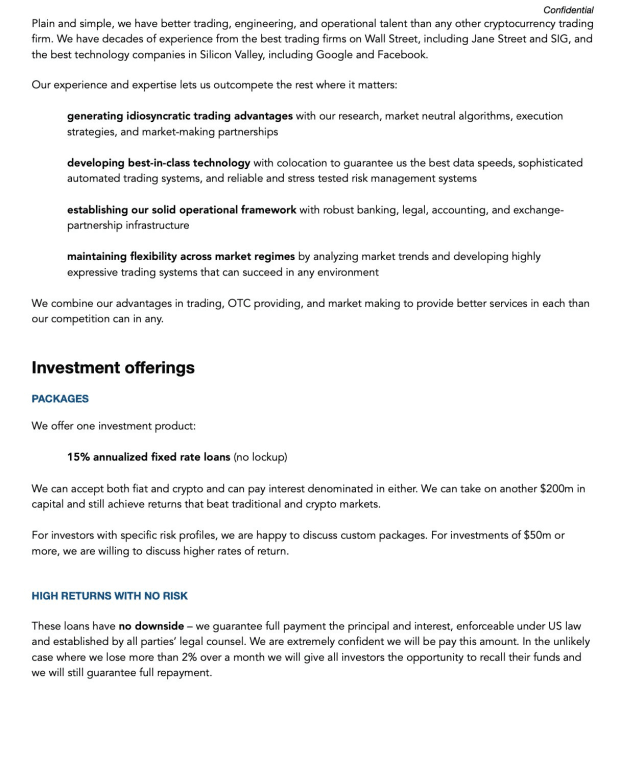

As the fallout of FTX unfolded, previous Alameda Research pitch decks from 2019 began to circulate, and for many the content was quite shocking. We will include the full deck below before diving into our analysis.

The deck contains many glaring red flags, including multiple grammatical errors, including the offering of only one investment product of “15% annualized fixed rate loans” that promise to have “no downside.”

All glaring red flags.

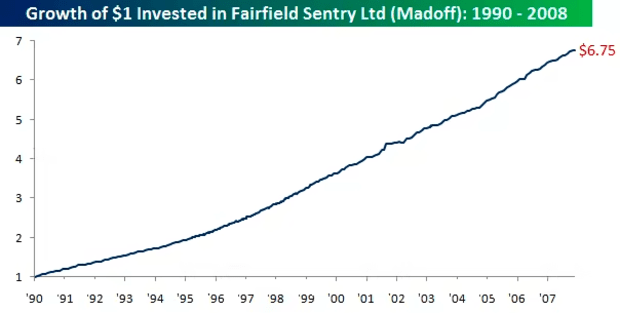

Similarly, the shape of the advertised Alameda equity curve (visualized in red), which seemingly was up and to the right with minimal volatility, while the broader cryptocurrency markets were in the midst of a violent bear market with vicious bear market rallies. While it is 100% possible for a firm to perform well in a bear market on the short side, the ability to generate consistent returns with near infinitesimal portfolio drawdowns is not a naturally occurring reality in financial markets. Actually, it is a tell-tale sign of a Ponzi scheme, of which we have seen before, throughout history.

The performance of Bernie Madoff’s Fairfield Sentry Ltd for nearly two decades operated quite similarly to what Alameda was promoting via their pitch deck in 2019:

- Up-only returns regardless of broader market regime

- Minimal volatility/drawdowns

- Guaranteeing the payout of returns while fraudulently paying out early investors with the capital of new investors

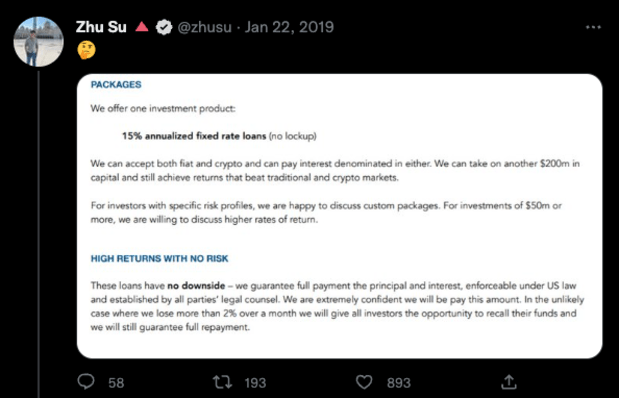

It appears that Alameda’s scheme began to run out of steam in 2019, which is when the firm pivoted to creating an exchange with an ICO (initial coin offering) in the form of FTT to continue to source capital. Zhu Su, the co-founder of now-defunct hedge fund Three Arrows Capital, seemed skeptical.

Approximately three months later, Zhu took to Twitter again to express his skepticism about Alameda’s next venture, the launch of an ICO and a new crypto derivatives exchange.

“These same guys are now trying to launch a "bitmex competitor" and do an ICO for it. 🤔” - Tweet, 4/13/19

Beneath this tweet, Zhu said the following while posting a screenshot of the FTT white paper:

“Last time they pressured my biz partner to get me to delete the tweet. They started doing this ICO after they couldn't find any more greater fools to borrow from even at 20%+. I get why nobody calls out scams early enough. Risk of exclusion higher than return from exposing.” - Tweet, 4/13/19

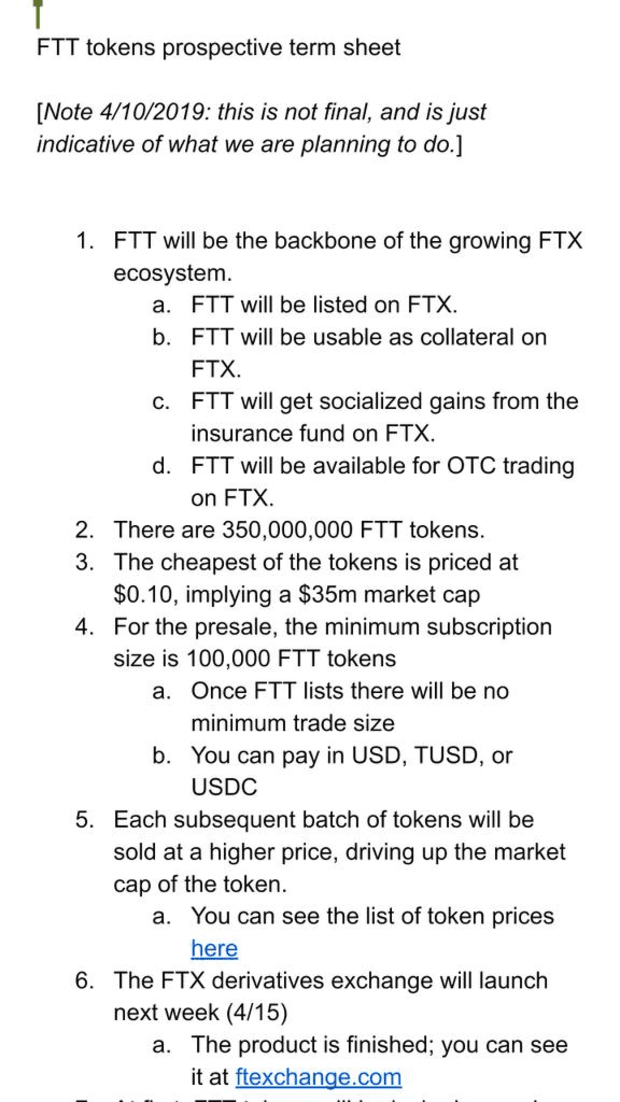

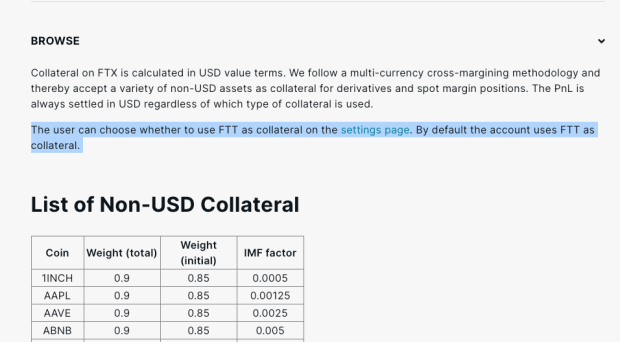

Additionally, FTT could be used as collateral in the FTX cross-collateralized liquidation engine. FTT received a collateral weighting of 0.95, whereas USDT & BTC received 0.975 and USD & USDC received a weighting of 1.00. This was true until the collapse of the exchange.

FTT Token

The FTT token was described as the “backbone” of the FTX exchange and was issued on Ethereum as a ERC20 token. In reality, it was mostly a rewards based marketing scheme to attract more users to the FTX platform and to prop up balance sheets. Most of the FTT supply was held by FTX and Alameda Research and Alameda was even in the initial seed round to fund the token. Out of the 350 million total supply of FTT, 280 million (80%) of it was controlled by FTX and 27.5 million made their way to an Alameda wallet.

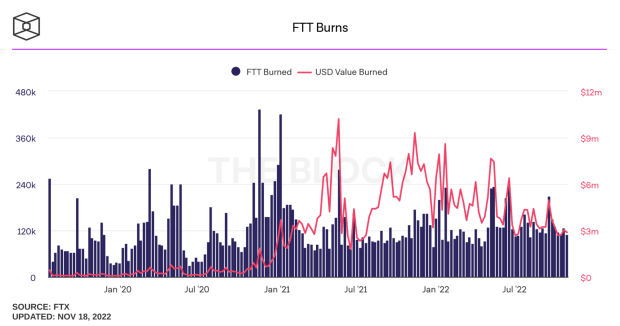

FTT holders benefited from additional FTX perks such as lower trading fees, discounts, rebates and the ability to use FTT as collateral to trade derivatives. To support FTT’s value, FTX routinely purchased FTT tokens using a percentage of trading fee revenue generated on the platform. Tokens were purchased and then burned weekly to continue driving up the value of FTT.

FTX repurchased burned FTT tokens based on 33% of fees generated on FTX markets, 10% of net additions to a backstop liquidity fund and 5% of fees earned from other uses of the FTX platform. The FTT token does not entitle its holders to FTX revenue, shares in FTX nor governance decisions over FTX’s treasury.

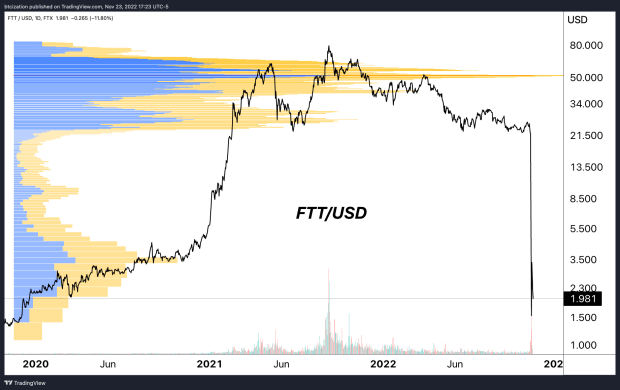

Alameda’s balance sheet was first mentioned in this Coindesk article showing that the fund held $3.66 billion in FTT tokens while $2.16 billion of that was used as collateral. The game was to drive up the perceived market value of FTT then use the token as collateral to borrow against it. The rise of Alameda’s balance sheet rose with the value of FTT. As long as the market didn’t rush to sell and collapse the price of FTT then the game could continue on.

FTT rode on the backs of the FTX marketing push, rising to a peak market cap of $9.6 billion back in September 2021 (not including locked allocations, all the while Alameda leveraged against it behind the scenes. The Alameda assets of $3.66b FTT & $2.16b “FTT collateral” in June of this year, along with its OXY, MAPs, and SRM allocations, were combined worth tens of billions of dollars at the top of the market in 2021.

CZ Chooses Blood

In one decision and tweet, CEO of Binance, CZ, kicked off the toppling of a house of cards that in hindsight, seems inevitable. Concerned that Binance would be left holding a worthless FTT token, the company aimed to sell $580 million of FTT at the time. That was bombshell news since Binance’s FTT holdings accounted for over 17% of the market cap value. This is the double edged sword of having the majority of FTT supply in the hands of a few and an illiquid FTT market that was used to drive and manipulate the price higher. When someone goes to sell something big, value collapses.

As a response to CZ’s announcement, Caroline of Alameda Research, made a critical mistake to announce their plans to buy all of Binance’s FTT at the current market price of $22. Doing that publicly sparked a wave of market open interest to place their bets on where FTT would go next. Short sellers piled in to drive the token price to zero with the thesis that something was off and the risk of insolvency was in play.

Ultimately, this scenario has been brewing since the Three Arrows Capital and Luna collapsed this past summer. It’s likely that Alameda had significant losses and exposure but were able to survive based on FTT token loans and leveraging FTX customer funds. It also makes sense now why FTX had an interest in bailing out companies like Voyager and BlockFi in the initial fallout. Those firms may have had large FTT holdings and it was necessary to keep them afloat to sustain the FTT market value. In the latest bankruptcy documents, it was revealed that $250 million in FTT was loaned to BlockFi.

With hindsight, now we know why Sam was buying up all of the FTT tokens he could get his hands on every week. No marginal buyers, lack of use cases and high risk loans with the FTT token were a ticking time bomb waiting to blow up.

How It All Ends

After pulling back the curtain, we now know that all of this led FTX and Alameda straight into bankruptcy with the firms disclosing that their top 50 creditors are owed $3.1 billion with only a $1.24 cash balance to pay it. The company likely has over a million creditors that are due money.

The original bankruptcy document is riddled with glaring gaps, balance sheet holes and a lack of financial controls and structures that were worse than Enron. All it took was one tweet about selling a large amount of FTT tokens and a rush for customers to start withdrawing their funds overnight to expose the asset and liability mismatch FTX was facing. Customer deposits weren’t even listed as liabilities in the balance sheet documents provided in the bankruptcy court filing despite what we know to be around $8.9 billion now. Now we can see that FTX never had really backed or properly accounted for the bitcoin and other crypto assets that customers were holding on their platform.

It was all a web of misallocated capital, leverage and the moving of customer funds around to try and keep the confidence game going and the two entities afloat.

.

.

.

This concludes an excerpt from “The FTX Ponzi: Uncovering The Largest Fraud In Crypto History.” To read and download the full 30-page report, follow this link.

source https://bitcoinmagazine.com/business/sam-bankman-fried-and-ftx-largest-crypto-fraud-history

Post a Comment